Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

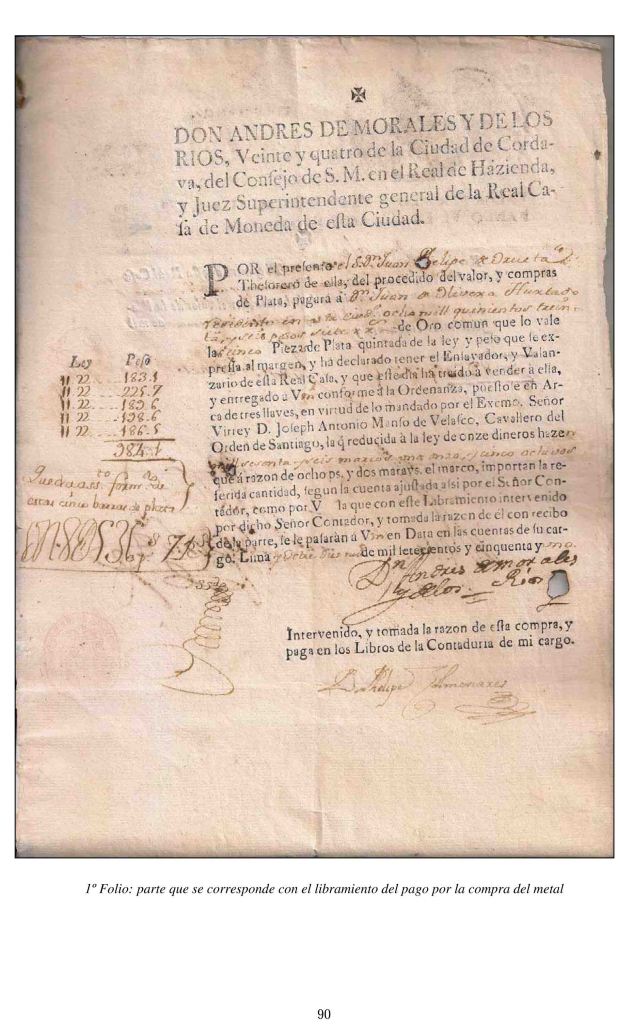

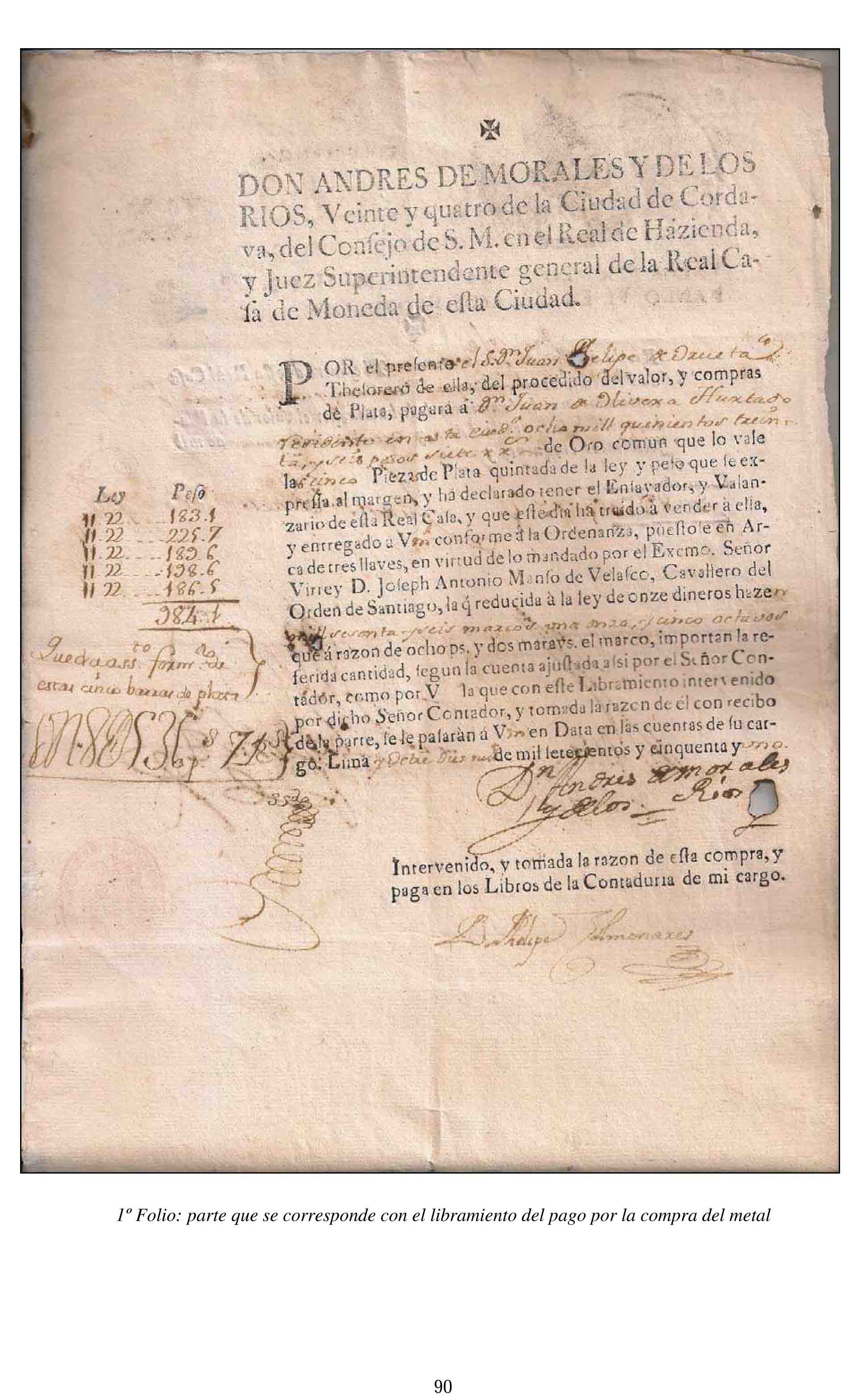

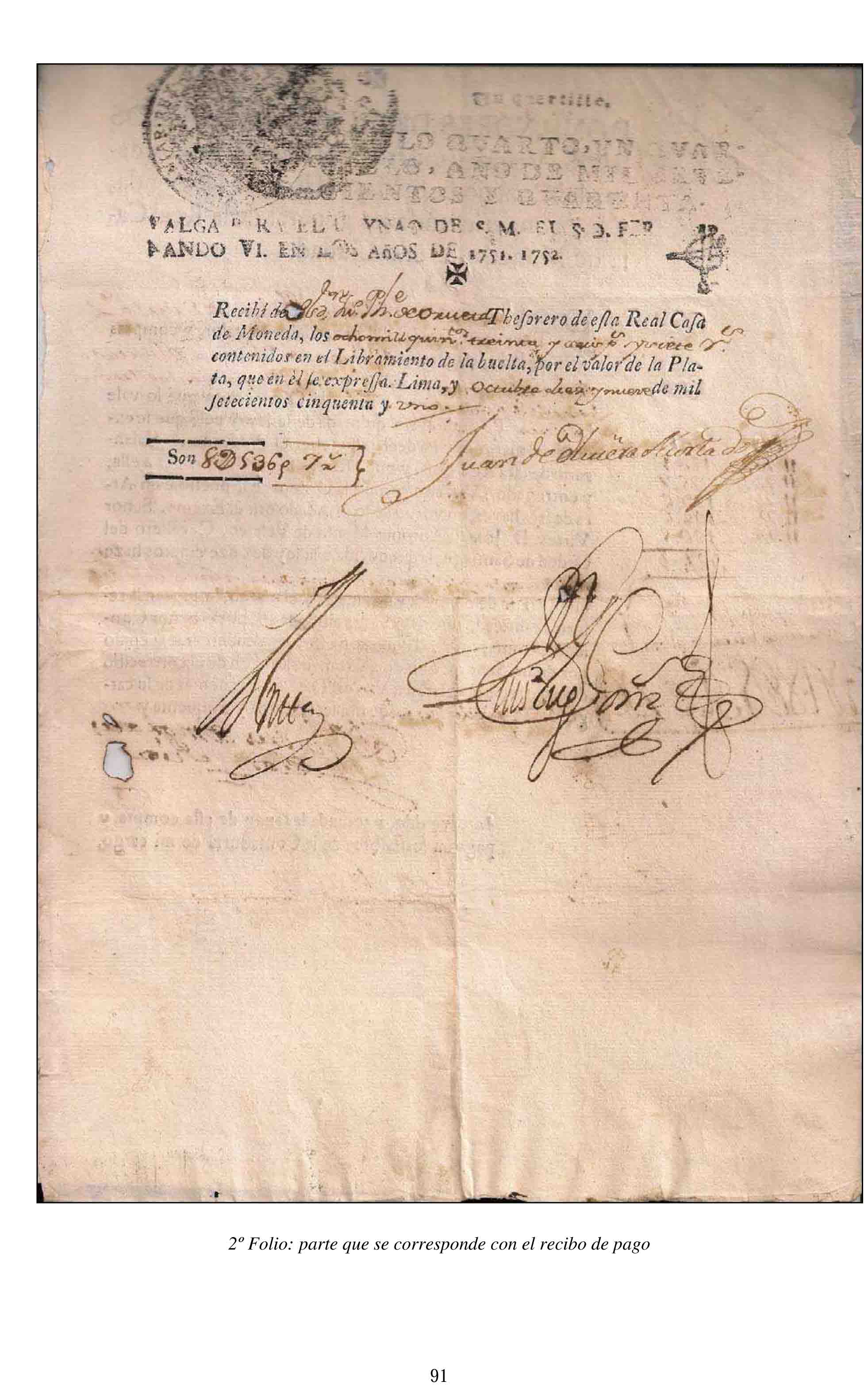

Vamos con la última parte. Además de pantógrafo y medallas, interesante testimonio de pantografista de la CECA (Casa de Moneda) de Lima

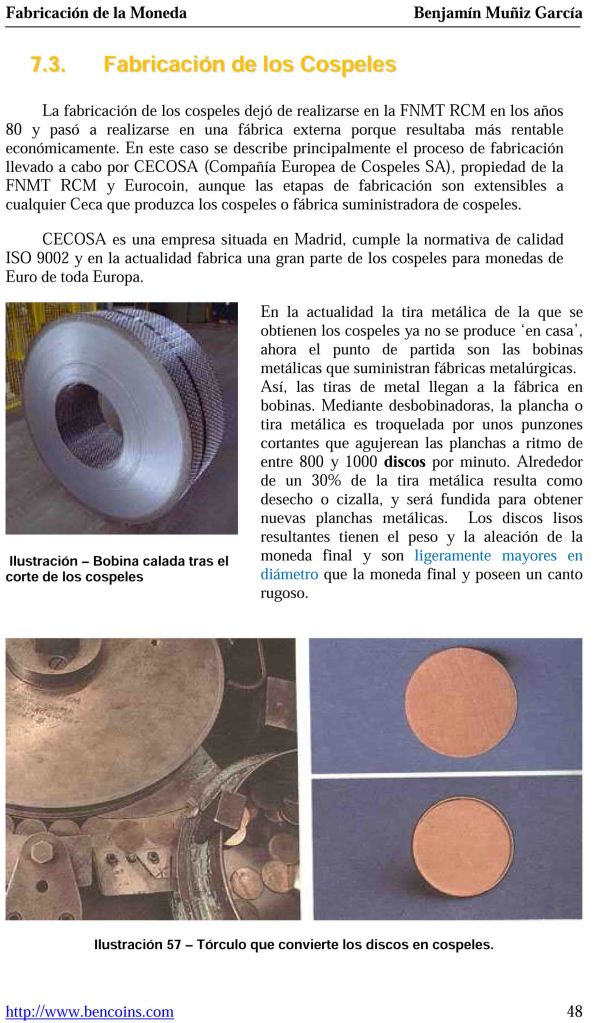

Situando el ratón sobre la imagen y pulsando botón derecho podéis abrir la imagen en pestaña aparte para ampliación/mejor lectura

Prensa de acuñación actual, ilustraciones, bibliografía y Glosario

Ilustraciones y Bibliografía la consultáis en el documento al final de esta entrada

Desafortunadamente, ni los vídeos detallados en el documento ni la descarga gratuita del libro son accesibles desde la página web de bencoins / UCM. He comprobado algunos enlaces que si funcionan

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Ya está aquí el verano, con todo lo que ello implica en cuanto a tiempo disponible, actividad, descanso, reflexión…

Un amable lector me indica que, a veces, mis textos son TL;DR (demasiado largo; no leído) Respetando todas las indicaciones/consejos/propuestas que recibo, debo decir que prefiero leer un texto una hora que ver un vídeo con la misma duración, entendiendo las actuales limitaciones de los más jóvenes y los no tanto para fijar su atención más de diez (10) minutos en lo que sea. Lo anterior no es una crítica; es un hecho. Los textos bien escritos reflexionan, condensan y fundamentan el tema tratado, negro sobre blanco, pudiendo releer por partes/subrayando lo buscado/de interés para el lector. Por contra, la linealidad de los vídeos hace que el espectador se deje llevar cómodamente entre imágenes y palabras de principio a fin. Un caso particular de lo anterior son las conferencias, sesudas o no; si es de más de media hora y el tema me interesa, prefiero leerla tranquilamente, por supuesto después de asistir al evento y haber preguntado lo que no haya entendido, en caso de haber turno de preguntas que, desgraciadamente, cada vez es menos frecuente en ciertos ámbitos/temáticas/contextos. Añado: hay malos textos y buenos vídeos, por supuesto; en cualquier caso, dependerá de hábitos/intereses/situaciones…

Por lo comentado en la primera línea de esta entrada, estoy dándome cuenta que la mal llamada inteligencia artificial (IA) se nutre gratis del trabajo de mucha gente en la red para dar resultados mediocres, con un coste elevado…pero ya iré ampliando estos meses de asueto mis divagaciones/experiencias

A lo que vamos: Sencillos y piezas de a ocho. El problema de la moneda de baja denominación en el Nuevo Reino de Granada en la segunda mitad del siglo XVIII/ Sencillos and Pieces of Eight. he Issue of Low Denomination Coinage in New Kingdom of Granada during the Second Half of the 18th Century

Resumen Uno de los desafíos para el buen funcionamiento del sistema monetario de las colonias españolas fue la provisión de monedas de baja denominación. El presente artículo analiza el problema de la aparente escasez de este tipo de moneda y su impacto en la eficiencia de la economía neogranadina. Para ello, se construyeron los detalles de emisiones de las dos casas de moneda del Reino y se analizaron los mecanismos de intercambio en las pequeñas transacciones. Se encontró que la Nueva Granada emitió monedas de baja denominación en mayores cantidades que otras cecas del mundo español en América, lo que le permitió tener un conjunto de medios de pago más equilibrado y mucho más adecuado para los pequeños intercambios. De esta manera, su economía presentó menores costos de transacción y fue, en cierto sentido, más eficiente.

Palabras clave: historia monetaria, economía colonial, moneda, Nuevo Reino de Granada.

Abstract One of the challenges for a well-functioning monetary system in the Spanish colonies was the supply of low denomination coinage. his article analyzes the problem of the apparent scarcity of this type of coinage, and its impact on the eiciency of the economy in New Granada. To accomplish this, it was necessary to construct a detailed account of issuances from the two mints in the Viceroyalty of New Granada and analyze the mechanisms of exchange for small transactions. Findings show that New Granada issued greater quantities of low denomination currency than other areas in Spanish America. This allowed for more stable forms of payment which were better suited for small transactions. Herefore, the economy of New Granada featured lower transaction costs and, in many ways, functioned more eficiently.

Keywords: monetary history, colonial economy, currency, New Kingdom of Granada.

Lo de colonias no es cierto; fueron provincias de ultramar

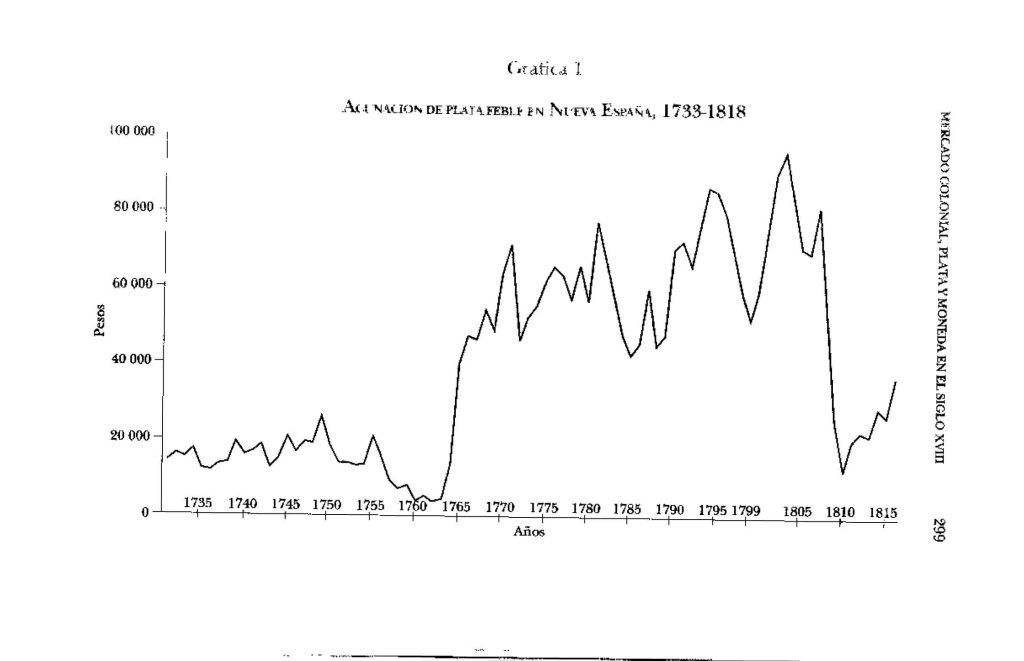

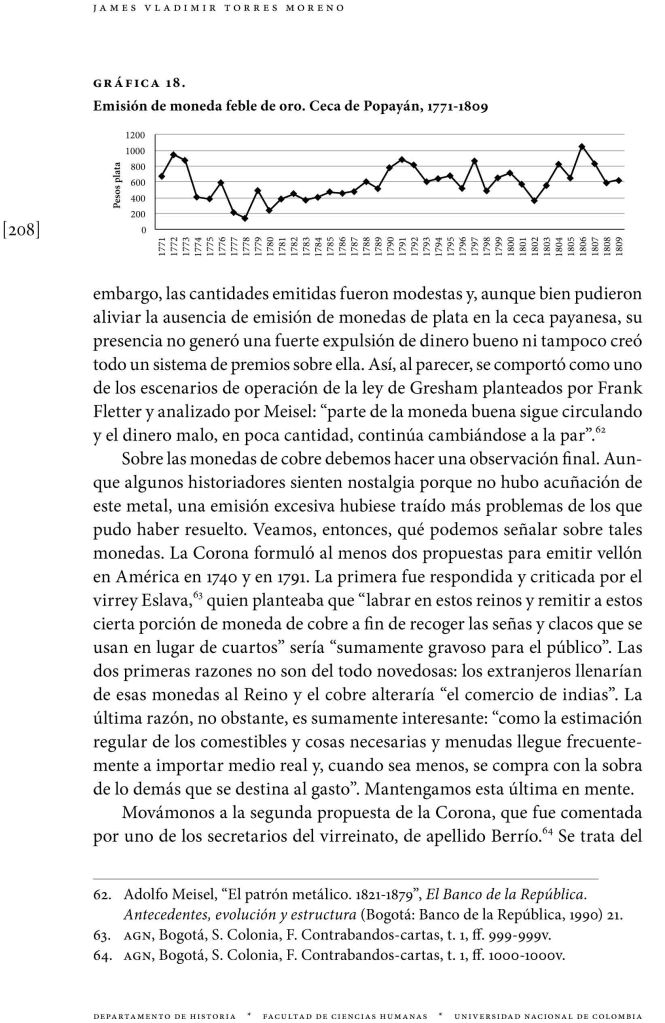

Este texto se refiere tanto a oro (Au) como a plata (Ag). Yo sólo pondré datos de la plata y al final de la entrada os dejaré el documento completo para vuestro estudio

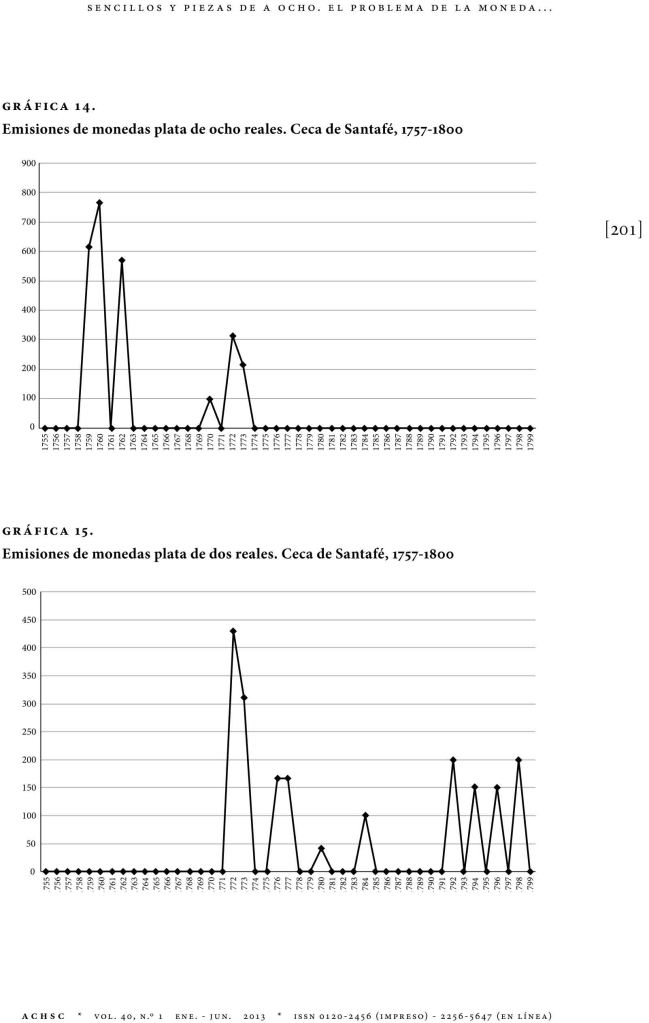

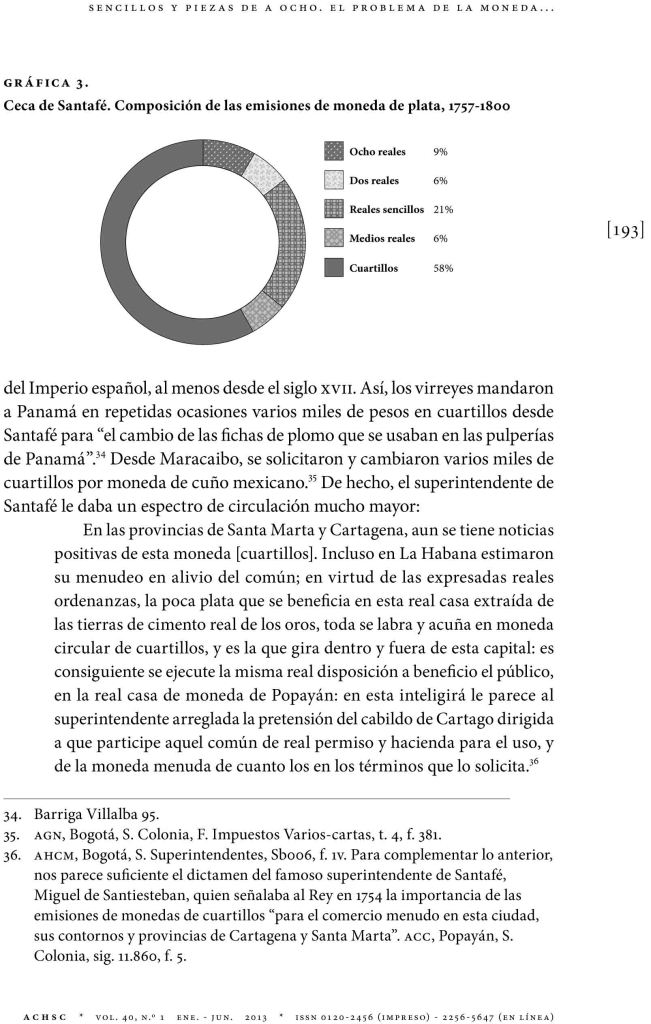

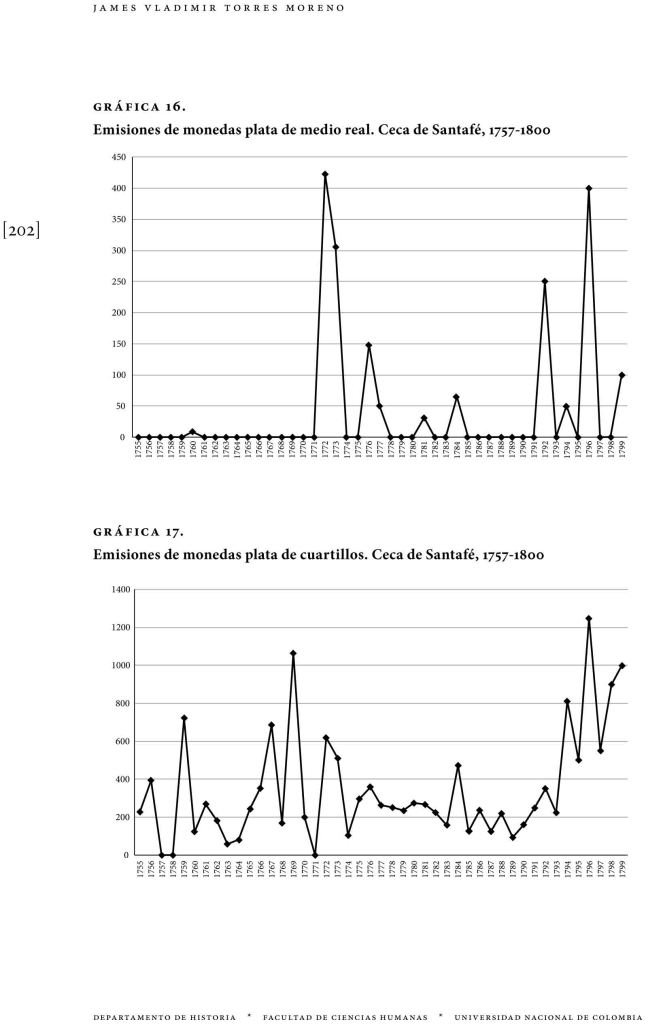

La CECA superior es la de Santa Fé de Nuevo Reino. En Popayán se acuñó mucha menos plata.

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

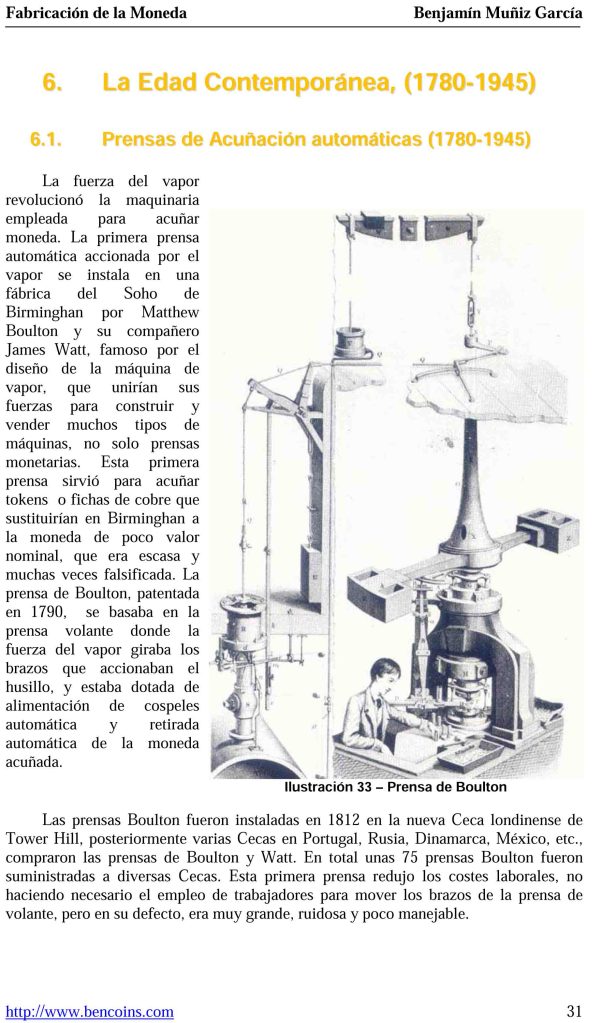

Ya en la Edad Contemporánea , aparecen las prensas de acuñación automática, detallándose varios fabricantes y las características técnicas de cada una.

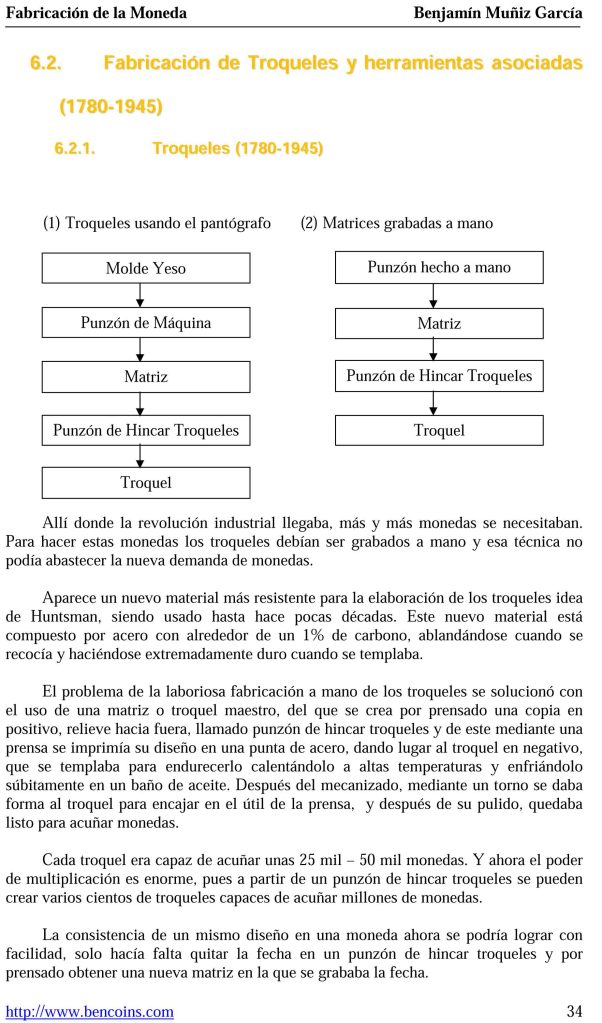

Punzones y troqueles para los nuevos tiempos. Pantógrafo, virola…

Situando el ratón sobre la imagen y pulsando botón derecho podéis abrir la imagen en pestaña aparte para ampliación/mejor lectura

Os dejo las últimas páginas completas de este capítulo

En la próxima entrada: Fabrica Nacional de Moneda y Timbre – Real Casa de la Moneda FNMT RCM

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Convención de Antequera junio 2026, un clásico de este blog 😉

Poco que añadir a lo dicho en multitud de entradas anteriores al respecto. Mismo hotel, misma sala, casi los mismos comerciantes y público asistente…material diverso y variado, eso si; moneditas para todos los gustos y bolsillos

Evidentemente, yo iba a lo mío, ya sabéis, además de saludar a viejos conocidos y resolver alguna duda sobre reales de a ocho y rusas. Tan importante es saber lo que compras como a quien comprárselo. Nunca me cansaré de repetir lo importante que es acudir a este tipo de eventos.

Mirando bandejas, selecciono este par de monedas

Ese 1813 de Madrid con busto de Fernando VII es rarillo aunque también lo es el 1812; comentando con el vendedor dejamos en tablas la rareza de ambos años, dejando claro que el 1813 tiene muchas variantes de ensayadores (IG, IJ, GJ y variantes sobreinscritas de fecha y ensayadores)

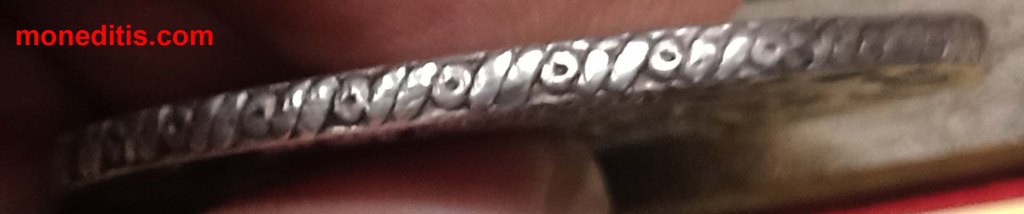

Canto de la limeña (fotos superiores), cadeneta círculo-cuadrado con superposición a 180º en el cerrillado, diferente al de la madrileña (fotos inferiores), dos barras-círculo con misma superposición de cerrillado (diferentes cantos americanas contra peninsulares)

La mañana va pasando y un comerciante me muestra este 3 rublos

Las fotos son malas y no subo el canto: la moneda es falsa. Da el peso pero el canto de cadeneta globular está demasiado bien hecho como para ser auténtica, entre otros múltiples detalles en anverso y reverso, poco apreciables en estas fotos.

Como no todo son monedas y antes de volver a casa, visito el Torcal de Antequera. ¡Im-presionante!

Día completo de experiencias varias. Hoy toca descansar.

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Sigo, más o menos, el mundo numismático subastero y de vez en cuando, dejo por aquí alguno/a de mis hallazgos/impresiones para vuestra consideración/análisis

Lot 29.BELGIEN. Brabant, Herzogtum. Albert und Isabella, 1598-1621.

Patagon o. J. (1612-1621), Tournai. 27.92 g. Vanhoudt 619 TO. Delmonte 260. Dav. 4438. Überdurchschnittlich gut ausgeprägt / Extraordinarily well struck. Sehr schön-vorzüglich / Very Fine-Extremely Fine. (~€ 440/USD 515)

Lot 42.BELGIEN. Brabant, Herzogtum. Philipp IV. von Spanien, 1621-1665.

2 Souverain d’or 1644, Brüssel. 11.09 g. Vanhoudt/Saunders 238. Delmonte 177. Fr. 106. Mit feinem Prägeglanz / With nice mint luster. Sehr schön-vorzüglich / Very Fine-Extremely Fine. (~€ 1’650/USD 1’925)

s/d. Felipe II. Potosí. B (Juan de Ballesteros Narvaez). 8 reales. (AC. 672). Valor: VIII. Escasa. 27,09 g. MBC-/BC+. Ex Colección Princesa de Eboli 20/10/2016, nº 142.

n/d. Felipe II. Potosi. B (Juan de Ballesteros Narvaez). 8 reales. (AC. 672). Value: VIII. Scarce. 27.09 g. MBC-/BC+. Ex Princess of Eboli Collection 10/20/2016, no. 142.

1758. Fernando VI. Lima. JM. 8 reales. (AC. 466). Columnario. Punto sobre las dos LMA. Bonito color. Escasa. 26,82 g. MBC+. Ex Áureo & Calicó 13/03/2008, nº 1180.

1758. Fernando VI. Lima. JM. 8 reales. (AC. 466). Columnario type. Dot over both LMA. Nice color. Scarce. 26.82 g. MBC+. Ex Aureo & Calicó 03/13/2008, no. 1180.

Lot 3218. Russia (USSR, Leningrad mint) Rouble 1924 – NGC MS 65

An outstanding lustrous exemplar with magnificent elegant toning.

Fedorin 9.

Despite being commonly encountered, it is rarely found in such a high state of preservation.

Siempre es interesante comparar precios entre monedas similares o iguales en unas y otras subastasnacionales/internacionales.

Cuidado con las comisiones de venta/martillo y los gastos de envío + posible burocracia de exportación u otros farragosos papeleosañadidos.

Los lotes de conjunto no se pueden devolver y con las monedas que no puedes valorar en mano siempre queda la duda/resquemorhasta recibirla en casa, no siendo siempre la conservación indicada por la casa de subastas la más fidedigna

P.S. Convención en Antequera el sábado que viene, 13 de junio, donde siempre. ¡Nos vemos!

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Libro también disponible en amazon / My book is also available in amazon amazon.com/.com.mx/.com.br/.co.uk/.co.jp/.com.au/.ca/.ie/.se/.de/.fr/.it/.nl/.pl + búsqueda / search Moneditis

Si; 1.000 entradas publicadas, 1.001 con esta…y parece que fue ayer cuando abrí este sitio.

Muchas situaciones, datos, momentos, experiencias, detalles… vienen a mi cabeza en este instante pero quizá sea mejor dejar esta entrada en blanco y que seáis vosotros los que repaséis este blog con la rueda del ratón/flechas de desplazamiento laterales/dedo sobre la pantalla táctil. O no.

Si llegáis hasta el principio os va a llevar un buen rato 🙂

Gracias

P.S. Entrada corta pero con enjundia

P.S.II aunque me ha costado un par de días pergeñar la celebración (el texto que habéis leído)